When it comes to investing in Canada, two accounts instantly come to mind: the Tax-Free Savings Account (TFSA) and the Registered Retirement Savings Plan (RRSP). Both offer powerful tax advantages. Both help build long-term wealth, but they work differently.

A common question people ask:

If I can’t maximize both right now, which one should I focus on first?

The answer depends on your situation, and timing can matter too.

For reference:

- March 2, 2026, is the deadline to make RRSP contributions for the 2025 tax year.

- TFSA contributions must be made by December 31 to count for the current calendar year.

Knowing these dates can help you plan your contributions strategically.

Quick Overview

TFSA

- Contributions are made with after-tax dollars

- Growth is tax-free

- Withdrawals are tax-free

- Withdrawals restore contribution room the following year

RRSP

- Contributions are tax-deductible

- Growth is tax-deferred

- Withdrawals are taxed as income Contribution room does not reset after withdrawal

The main difference is that a TFSA gives you the tax benefit later and a RRSP gives it to you now.

When a TFSA May Make More Sense

1. You’re in a Lower Tax Bracket

If you’re early in your career or earning less income, an RRSP deduction may not be especially valuable today. A TFSA allows tax-free growth without “using” your deduction at a lower rate.

2. You Want Flexibility

TFSA withdrawals:

- Are tax-free

- Don’t affect income-tested benefits

- Can be recontributed

That makes TFSAs ideal for emergency funds, major purchases, or career transitions.

3. You Expect Income to Rise

If you anticipate earning more in the future, saving your RRSP room for higher-income years could create a larger tax benefit later.

When an RRSP May Make More Sense

1. You’re in a Higher Tax Bracket

If you’re earning strong income today, RRSP contributions can meaningfully reduce taxes now. Reinvesting the refund can significantly boost long-term growth. With the March 2, 2026, deadline approaching for the 2025 tax year, this can be a useful planning opportunity.

2. You Expect to Retire in a Lower Tax Bracket

The RRSP works best when you:

- Contribute at a high tax rate

- Withdraw at a lower tax rate

That difference is what makes it powerful.

3. You Want Structured Retirement Savings

RRSPs are clearly earmarked for retirement. Withdrawals are taxable and later convert to a Registered Retirement Income Fund (RRIF) with minimum withdrawals, which creates discipline for some investors.

The Often-Overlooked Factors

Government Benefits

RRSP withdrawals count as income while TFSA withdrawals do not.

This can affect:

- Old Age Security (OAS)

- Guaranteed Income Supplement (GIS) eligibility

- Other income-tested benefits

Large RRSP balances can sometimes create higher taxable retirement income than expected.

Contribution Room

TFSA room is the same for everyone. RRSP room depends on earned income, meaning higher earners accumulate more. And remember, unused TFSA room carries forward indefinitely, while RRSP room also accumulates if unused, giving you flexibility to plan contributions around income peaks.

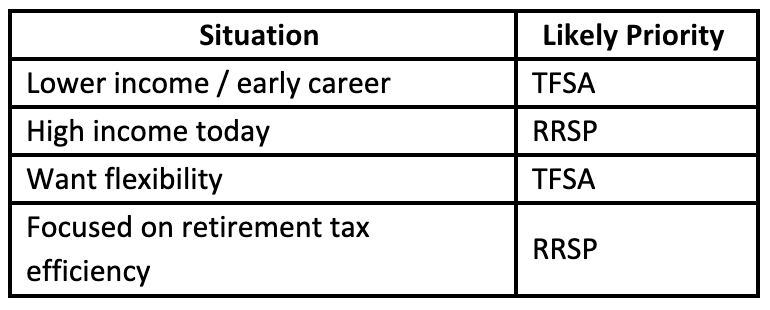

So… Which Should You Maximize First?

Here’s a simplified guide:

For many Canadians, the smartest strategy isn’t either/or, it’s sequencing:

- TFSA first, RRSP later

- Contribute enough to RRSP to drop tax brackets

- Invest your RRSP refund into your TFSA

- Use both strategically over time

Final Thoughts

This isn’t about “winning” the TFSA vs. RRSP debate. It’s about being intentional.

Ask yourself:

- What tax bracket am I in today?

- Do I expect my income to increase?

- Do I value flexibility?

- Would I reinvest my RRSP refund, or spend it?

- Am I approaching a contribution deadline I can use strategically?

Early in your career, flexibility may matter most. Mid-career, tax efficiency may take priority. Closer to retirement, income planning becomes key.

These small structural decisions compound, just like investments do.

If you’re unsure which account deserves priority in your situation, it may be worth having a conversation with your financial advisor to make sure both are working together, not just individually.

Whether you're a current client or someone looking to take the next step toward financial success, Alpen Investment Advisors is here to guide you every step of the way. Based in North Vancouver, our team, led by Jon Alpen, brings over 20 years of experience in helping clients grow, preserve, and navigate their wealth. With expert guidance, tailored solutions, and a steadfast commitment to your success, we are dedicated to supporting your unique financial journey.

Reach out to us today at jonathan@alpenia.ca to start or continue building your financial future with confidence and clarity.